Designing Investment Policy for ESG and Impact Investing

By Loren Francis on October 24th, 2017

“We believe that considering material ESG factors as part of our investment decision-making process, with respect to both direct and indirect investments, along with other material investment factors is consistent with our fiduciary duty”.

– UTAM

There is a mind shift underway in the evolution of fiduciary duty in the world of investing: a move away from the old school thinking of “maximizing returns” without regard to impact and exercising due care, to one of skill and diligence by way of Environmental, Social and Governance (ESG) factor analysis that our fiduciary obligations requires us to consider. Ultimately, using our capital to shape a better society.

At the same time and on the other side of the table, companies are facing an increased pressure for better disclosure of what they are actually doing to address ESG factors in their business to enhance sustainability. As Elisse Walter of the Sustainability Accounting Standards Board (SASB) so eloquently states in her speech at a March 2017 CPA Canada Event, markets are being reshaped by resource constraints, climate change, population growth, technological innovation, and globalization. Sustainability is poised to be the next competitive frontier. In fact, research has already shown that companies can achieve superior results—including return on sales, sales growth, return on assets, and return on equity, in addition to improved risk-adjusted shareholder returns—by focusing on the limited number of materiality-based, industry-specific sustainability topics as identified by SASB. The question is no longer whether companies should disclose information on material sustainability risks and opportunities; it is how they can improve the effectiveness of the disclosures they are already making.

In short, it is not about more disclosure; it is about better disclosure. Many are promoting and supporting corporate environmental disclosures with a focus on climate. Most recently, over management’s objections, shareholder resolutions to disclose climate risks passed at the annual meetings of ExxonMobil and Occidental Petroleum this past May.

So how should we as investors, think about making our world a better place and align ourselves with the United Nations sustainable goals to end poverty, protect the planet and ensure prosperity for all? How can we design our Investment Policy to align with what we believe in?

Responsible Investing

Responsible Investing is an approach that integrates consideration of ESG matters into investment activities with the objective of enhancing long term investment performance.

The integration of ESG considerations within investment processes and across asset classes continues to gain interest among investors and concerned citizens. Evaluation of ESG factors can provide insights into investment risk and management of ESG risks can add to long term sustainable returns. Studies have shown that companies with robust sustainability practices demonstrate better operational performance. Strong corporate environmental performance also links to financial outperformance. Strong ESG standards correlate with good stock price performance, and of course, brand awareness. We all know that poor governance, or poor health and safety measures, or exploitive labour practices directly impacts shareholder value (think emissions scandals, or non-compliance with building codes resulting in collapse).

Investment policies surrounding Responsible Investing are being considered and developed by investors, families and foundation investment committees. There is no “right” way, but the best way is to incorporate policies into an Investment Policy Statement (IPS) that communicates the investor’s wishes and beliefs. Some choose to develop a Responsible Investment Policy to be housed within a section of the IPS or as an addendum to an IPS. Either way, a policy formalizes the practice of integrating ESG issues into investment decision making. An addendum to the IPS may be a simple way to start as to how to include ESG factors. As we move forward, Responsible Investing may become incorporated throughout the IPS.

ESG Issues to Consider:

Examples of Responsible Investment Policies

As per the PRI guide on writing a Responsible Investment Policy, policies can take many different shapes. You might start by identifying high level core beliefs that are central to you, and you might read other IPS’s that have been designed for ESG and Social Impact Investing.

For example, the Western University IPS states a belief that ESG factors may have an impact on corporate performance over the long term. Section 4 of its IPS, titled Responsible Investing, outlines how the university will engage external investment managers and that this engagement will involve increasing the level of scrutiny on ESG factors. The university will keep a registry, updated annually as to ESG related information on its external managers. This may include incorporation of ESG factors into the firm’s investment process, the firm’s target allocation for climate change related investments, the presence of a committee on sustainable investment, the portfolio’s exposure to fossil fuels, sustainable industries, and high impact sectors, and details about the firm’s proxy voting policy.

Another great example is the University of Toronto’s (U of T) annual report on Responsible Investing. U of T has a major commitment to Responsible Investing and in particular, points to a comprehensive approach to the challenges posed by climate change. The University president, Meric Gertler, called on the University Pension committee to incorporate ESG factors into its Statement of Policies and Procedures, a change that was implemented in June 2016. He also called on UTAM (the University of Toronto Asset Management Group) to build a rigorous and systematic approach to integrating ESG factors into investment decisions. UTAM, along with many other universities and investment managers, is now a signatory to the United Nations supported 6 Principles for Responsible Investment (PRI):

- We will incorporate ESG issues into investment analysis and decision-making processes.

- We will be active owners and incorporate ESG issues into our ownership policies and practices.

- We will seek appropriate disclosure on ESG issues by the entities in which we invest.

- We will promote acceptance and implementation of the Principles within the investment industry.

- We will work together to enhance our effectiveness in implementing the Principles.

- We will each report on our activities and progress towards implementing the Principles.

Putting It in Perspective: Sustainable Investment Taxonomy

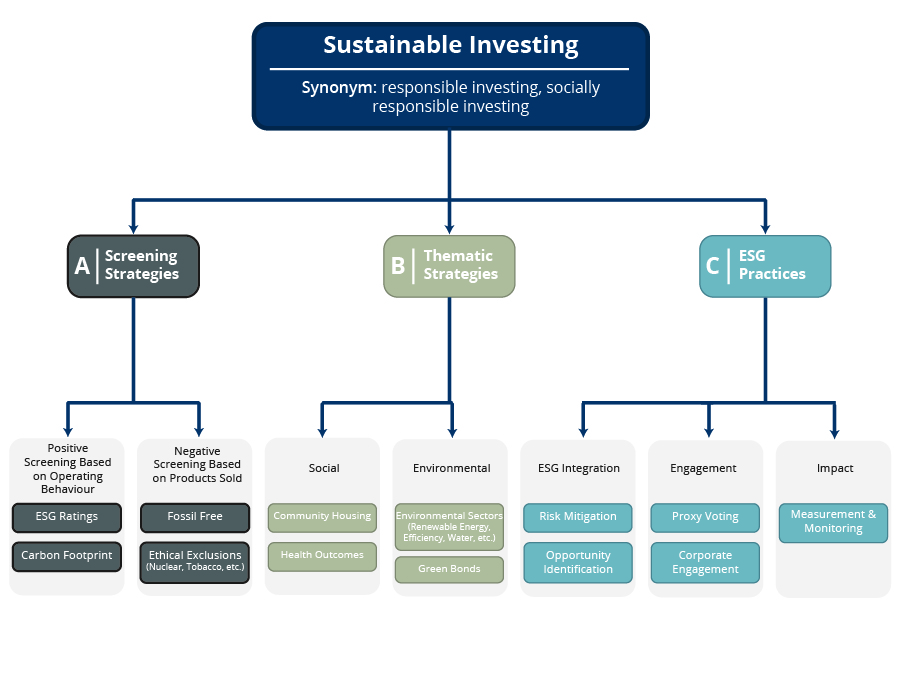

An excellent model on describing the matrix of Responsible Investing can be found in the TASK FORCE Report on Sustainable Investment Taxonomy: September 2016. This report describes Responsible Investing or Socially Responsible Investing as being synonymous with sustainability and it provides for a simple model on the taxonomy of sustainable investing, dividing it into three distinct orders:

- Screening Strategies:

Screening Strategies can be negative or positive. Negative screening would simply exclude companies based on what they sell such as tobacco, alcohol, weapons, gambling, pornography, or fossil fuel. Positive screening involves identifying companies that have a positive impact, and often use ESG measurement systems and scores to guide decisions. MSCI and Morningstar/Sustainalytics are providers of measurement and scoring systems used by many investment managers today.

- Thematic Strategies:

Thematic Strategies are built on focussed and constrained investment universes. Thematic strategies will have very specific allocations and can typically be overexposed to some sectors such as clean technology, renewable energy, industrial and technology, and underexposed to sectors such as energy, financials, or consumer.

- ESG Practices:

ESG Practices are not an investment strategy per se, but a group of investment practices. They are not the primary driver of an investment thesis but rather practices of making investment decisions. ESG integration is currently being employed by many traditional investment managers as a way to identify new business risks, and improve corporate behaviour through direct engagement and shareholder activism. According to the Responsible Investment Association (RIA), 80% of investment managers now pay attention to ESG issues.

ESG factors include climate change, biodiversity, air and water pollution, corruption, executive remuneration, and board diversity among others. These are all material issues that should be integrated into the investment making decision processes. Voting can affect governance, and provide a management team with valuable feedback. Important voting issues should be reviewed and voting rights used in a responsible way so as to add value to change.

ESG Practices and Designing Your Own Investment Policy Statement

There are three primary ESG Practices:

- Identifying emerging ESG risks.

- Actively influencing the operating behaviour of management teams through engagement strategies, proxy voting, corporate engagement and shareholder activism.

- The measurement and monitoring of environmental and social impact.

In designing your own Investment Policy Statement, and incorporating Responsible Investment guidelines you may want to think about:

- Incorporating ESG standards for investments. These could be high level, or specific based on certain issues and minimum standards.

- Your core beliefs such as companies need quality management, strong, diverse and effective boards, transparent shareholder reporting, recognition of environmental and social risks, and executive compensation that aligns well.

- Setting guidelines for ESG practices across all asset classes. Research has shown that governance scores are most important when determining bond credit worthiness. Bonds with high governance scores suffer credit downgrades less often.

- Setting guidelines for working with external investment managers; what issues are important, what requirements and measurements are expected.

- Social or environmental themes that may be important to you such as community housing, clean technology, climate, food, agriculture and forestry, green investing, renewable resources, social impact bonds, waste management and/or water infrastructure and technology. You may wish to review the UN Sustainable Development Goals for further background and understanding.

As described in the Taxonomy model, potential approaches for responsible investing can include negative and/or positive screening, theme investing or ESG integration. You may wish to invest through the traditional public markets or through private markets. You might combine some of the approaches or all of the approaches.

As mentioned earlier, there is no “right” way but rather the way that suits your individual, family or foundation goals and objectives.

Moving Towards a 100% Impact Portfolio

Certain organizations are moving proactively and intentionally toward a 100% impact portfolio where all of their assets are used to generate positive impact. Inspirit Foundation is one such organization. The mission of the Inspirit Foundation is to promote inclusion and pluralism through media and arts, provide support for young change leaders and impact investing—specifically addressing discrimination based on ethnicity, race and religion. The Inspirit Foundation believes it can create positive change through their capital allocation and is on the road towards a 100% Impact Portfolio. They are not the first foundation to think this way and they acknowledge the work that has been done before them by foundations such as the F.B. Heron Foundation, The Hamilton Community Foundation and the Edmonton Community Foundation.

The Inspirit Foundation believes in using financial capital to support companies that behave responsibly and they will engage and respectfully challenge companies that have room for improvement. For Inspirit, the definition of 100% Impact includes:

- Applying impact investing tools to the public portfolio (90% of the portfolio) by incorporating positive screening and ESG factors into mainstream traditional investments, ensuring shareholder engagement, having some specific product choices (i.e. shift capital to renewable energy sources through a fossil fuel free equity fund), and by not knowingly investing in alcohol, gambling, pornography and adult entertainment, tobacco and related products and weapons.

- An allocation of 10% to private investments that contribute to inclusive society through mission and program related investment. This is invested by way of private real estate, private debt and private equity.

While Impact investing is not new, it continues to grow in interest and capture attention across the investment community. At HighView, we began our journey through research and meeting with many people and firms that focus their time and energy on sustainable investing. HighView joined the Responsible Investment Association (RIA) this past spring, and more recently, our Portfolio Strategy Committee has enhanced our investment manager selection and ongoing monitoring processes by implementing an ESG due diligence component to understand how our managers integrate ESG factors into their investment research. While only a start, we will continue to look for ways to bolster our expertise and capabilities in this burgeoning sector.

To that end, HighView works strategically and collaboratively with firms that have specific expertise beyond our own. In this regard, we are pleased to align with Purpose Capital. Formed in 2010, Purpose Capital is an impact advisory firm that designs and deploys customized impact investment strategies by mobilizing all forms of capital to accelerate social progress. Purpose Capital has worked extensively with Inspirit Foundation on their impact investment journey. We are excited to continue our focus in exploring new ideas for sustainable investing, and stepping beyond ESG integration to meet our clients’ evolving requirements.

Sources

- TASK FORCE on Sustainable Investment Taxonomy, September 2016: http://greenchipfinancial.com/wp-content/uploads/sites/5/2016/09/Sustainable-Investment-Taxonomy-Report.pdf

- University IPS’s: http://www.intentionalendowments.org/investment_policy_statements

- SUSTAINABILITY MATTERS: FOCUSING ON YOUR FUTURE TODAY, By Elisse B. Walter

SASB Board Member and Former Chair of the SEC

CPA Canada Event, March 30, 2017

https://www.sasb.org/blog-elisse-walters-keynote-at-cpa-canada-conference/

Special thanks to Hyewon Kong and Nadi Naderi of AGF Investments, to Julie Desjardins of RIA, and to Upkar Arora, CEO of Purpose Capital for their knowledge and guidance on Sustainable Investing.

HighView is an experienced portfolio management firm for affluent Canadian families and foundations. We would be happy to discuss our goals-based investment approach with you and your professional advisors.

You may also be interested in: