“We will be known forever by the tracks we leave.” – Dakota Proverb

“We will be known forever by the tracks we leave.” – Dakota Proverb

On September 25th 2015, the United Nations (UN) with countries around the world adopted a set of goals to end poverty, protect the planet, and ensure prosperity for all as part of a new sustainable development agenda. As the UN believes, sustainable development is defined as meeting the needs of the present without compromising the ability of future generations to meet their own needs; sustainability is a global imperative and investors are essential partners in its achievement.

Investors have a role to play in addressing social challenges. All investments have an impact on our environment and community. We can play a part in ensuring a more sustainable environment through the investment decisions we make. Aligning our values with investment to include both a financial return and a measurable social impact is referred to as a double bottom line. Increasing the flow of capital to investment strategies that generate a financial return while intentionally improving social and environmental conditions will benefit all of us.

Investing for Social Impact

Among our families and foundations there is a growing interest about investing for social impact. The theory of social impact investing has been around for some time but seems to have really taken root in 2006 when the UN launched the Principles for Responsible Investment (PRI).

Although not new to Canada, interest in social impact investing is accelerating. The investment spectrum is wide, from socially responsible investing (SRI) to environmental, social, and governance (ESG) to impact funds to direct impact investments or mission related investments (MRI) for endowment funds. There has been a significant movement underfoot as interest in both responsible investing and impact investing has gained traction.

Recognition that ESG issues are financially material is causing investors to demand more from their investments. As investors move to align their values with investment goals, and as social entrepreneurs seek to make a difference, direct impact investing is growing.

This upward trend is a result of increased opportunities and a greater demand due to growing awareness of environmental and social challenges. The concept of fiduciary duty for investing is morphing from one of financial return only to also include an understanding of how business impacts our environment and the footprint it leaves behind.

As Porter and Kramer so eloquently explain in their article “Creating Shared Value” (HBR Jan 2011), we need to move away from optimization of short term performance and overlooking the greater needs of society to achieve long term success. We need to reconnect company success with social progress and bring business and society back together. At the very least, companies should no longer maximize economic value without taking into account ESG issues.

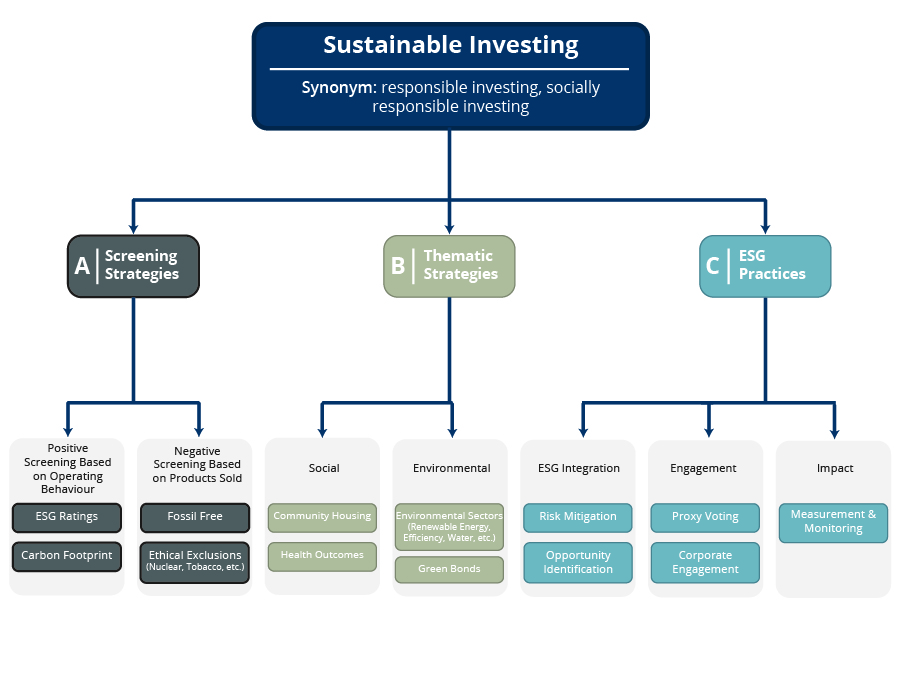

What Is SRI/ESG Investing?

SRI/ESG investing is made with environmental and social risks in mind but specific return from measurable social or environmental impact is not necessarily a required outcome. SRI/ESG investing focusses primarily on screening out or avoiding investment in harmful companies and encouraging improved corporate practices. There is a growing belief that companies with exceptional environmental and social programs will outperform in the longer term.

What Is Impact investing?

Impact investments on the other hand are investments made into companies, organizations, and funds with the intention to generate measurable, beneficial, social, and environmental impact along with a financial return, hence a double bottom line.

Impact investors want to move beyond SRI/ESG to investments that have social and environmental impact as a primary criterion. Impact investors may receive a range of returns depending on what their investment goals are. Some investments may be below market while providing a social benefit, while other investments can provide market returns with social impact.

Impact investments differ from traditional investments because of the strategy for creating social and environmental impact, and the financial return may be quantified by different risk return calculations. Impact investing may include direct investment into underserved communities or individuals, and debt or equity financing provided to businesses with an environmental or social purpose.

Incorporating Values Investing with Goals-based Investing

For both families and foundations, the passion for alignment of investments with values and beliefs is growing.

As part of a Goals-based Investing approach, questions may include:

- Alongside our personal or foundation goals, how do our investments reflect our sense of values and the impact we want to have?

- What social and environmental challenges are we interested in as a family?

- Do we have a responsibility to use wealth for the greater good of society?

- Should we allocate some of our investments to social impact?

- Should the fiduciary of our investment assets consider ESG or impact investing?

- Do any of our current investments conflict with our foundation goals or philosophies?

There are many ways that families and foundations can begin to incorporate impact investing into their Investment Policy Statement (IPS). Developing an impact investing strategy will depend on the motivations and objectives of the family or foundation.

It may begin with an allocation or carve out to SRI/ESG specific funds, or ensuring investment managers consider SRI/ESG factors when analyzing companies such as being proactive on factors like climate change, economic inequality, human rights, executive pay, supply chain management, or resource scarcity. Or it might include an allocation to direct social impact investments through funds or private debt or equity. It is anticipated that formal policies on impact investing will take shape in the not too distant future, if not already.

Social Impact Investing for Families

For families, including social impact investing as part of the family wealth vision can allow for healthy discussion and wealth transition among family members, particularly with the millennial generation.

Most millennials today believe that social impact is key to making investment decisions (US Trust 2016). In a recent Deloitte study, Millennials rank “improve society” as a number one priority for business. A survey by Merrill Lynch Private Banking suggests for millennials that a values-based approach is important and that environmental concerns are often a top priority.

For millennials, seeking achievement of social objectives alongside financial return is of great importance. My own introduction to social impact investing was through a former younger colleague of mine, Andrew Nobrega. Andrew was instrumental in my initial learning as he shared his passion for innovative social structure and strong business models that promoted aligned interests between business, investors, local communities, and the environment. He went on to pursue his passion by working for Pur Projet, a firm that promotes the livelihood and regeneration of global ecosystems.

For families considering the transition of a family business, this alignment of millennial aspirations of making a difference by way of social impact can play an important role in the future of the family business.

Social Impact Investing for Foundations

“Should a foundation be more than a private investment company that uses some of its excess cash flow for charitable purposes?” – F.B. Heron Foundation

For foundations, aligning goals of making society a better place with investments makes intuitive sense given their existence to leverage social change. Foundations are a natural fit given their focus on social issues. More and more foundations are rethinking their funding models in support of their philanthropic missions and increasing impact in their communities.

In addition to grant making, many foundations are allocating up to 10% of their endowed funds to social impact or mission related investing (MRI), with some foundations taking a significant lead like the Inspirit Foundation in Canada which has committed to achieving a “100% impact portfolio to help create a more inclusive and pluralist society”, and the F.B. Heron Foundation in the USA which is moving towards being fully invested in impact investments that address job creation.

MRI may be defined as using the endowment capital of the foundation to invest in companies, funds, or direct investments that generate both positive social or environmental impact as well as financial returns. The Canadian Task Force on Social Finance recommended that foundations should invest at least 10% of their assets in mission-related investments by 2020. This recommendation has been endorsed by both the Community Foundations of Canada (CFC) and the Philanthropic Foundations of Canada (PFC).

Social Impact Investing in Canada

In Canada, most impact investment capital is focused on the housing/real estate sector, and the clean technology sector (RIA Trends Report 2016) but impact investing also happens across a number of sectors including energy and resource efficiency, education, healthcare, Aboriginal, housing and community facilities, food and agriculture, environment and water, not for profit, and social enterprise.

Investments can be done through:

- Community Economic Development Investment Funds

- Community Loan Funds

- GICs

- Bonds and loans through financial institutions

- Social enterprise loans

- Social housing development

- Direct impact investments

- Private equity funds

- Venture funds

- Investment co-ops

- Labour sponsored funds

- Public equity funds

Interestingly, Ontario recently issued its first Social Impact Bond (SIB) in collaboration with the Heart and Stroke Foundation, The Public Health Agency of Canada, and the MaRS Centre for Impact Investing. A SIB, or ‘pay for success’ model, is not like a traditional bond – repayment depends on measured social outcomes. If objectives are not achieved, investors may not receive their money. The government repays investors with interest if the program meets its outcome targets. Pay for success is modelled on the belief that attaching payment to outcomes will drive better program design and execution.

Of course, social impact investing is not without its challenges – performance metrics and assessing net social benefits are not easily measured. There may be legal/CRA/regulatory issues to consider, specifically for foundations. Leadership and organizational development, business model execution and management, insufficient coverage, small deal sizes, transaction costs, lack of established track record, and fragmentation of the social impact investing universe can all present issues.

However, as knowledge and deal size grows, as track records are built, as methodologies for measuring social returns are defined, and as financial performance is realized, the space will continue to flourish. Improvements in the space are well underway as various companies and not-for-profit organizations such as IRIS, B Corporation, and Sustainalytics are establishing performance metrics, and platforms such as the Social Venture Connection (SVX) are developing for impact investments.

In Canada, we have a number of tremendous resources in regards to impact investing:

- The MaRS Centre for Impact Investing in Toronto: Works to unlock the power of private capital to tackle our toughest social challenges. MaRS works with governments, investors, service providers, and ventures to create funding solutions for projects that deliver real change.

- The Social Venture Connection (SVX): A private investment platform built to connect impact ventures, funds, and investors was developed under the leadership of MaRS in collaboration with the TMX Group. The SVX platform helps catalyze new debt and equity investment capital for ventures that have demonstrable social and/or environmental impact and the potential for financial return.

- The Responsible Investment Association (RIA): Canada’s membership association for Responsible Investment (RI). Members include mutual fund companies, financial institutions, asset management firms, advisors, consultants, investment research firms, asset owners, individual investors, and others interested in RI. RIA members believe that the integration of environmental, social, and governance (ESG) factors into the selection and management of investments can provide superior risk adjusted returns and positive societal impact.

On a global basis, as referred to earlier, Principles of Responsible Investment now has over 1600 signatories committed to six responsible investment principles. Global assets under management represented by the signatories of PRI is over $62 trillion. The Global Impact Investment Network (GIIN) and Impact Assets also both provide an excellent resource of information.

Commitment to create real sustained change requires collaborative action amongst all stakeholders. We all play a role in creating a more sustainable environment through our own actions and the investment decisions we make.

As our collective knowledge and experience expands, it is expected that social impact investing will grow in Canada. As suggested by the Canadian Task Force on Social Finance, mobilizing private capital to generate social and economic value represents an effective opportunity to address the capital requirements to advance solutions for Canada’s complex social and environmental challenges.

And on a global basis, impact investing will play a unique role in achieving the UN’s Sustainable Development Goals and building a sustainable future.

“There can be no Plan B because there is no Planet B.” – UN secretary General Ban Ki-moon

A Transformation in the Investment Management Industry

As the momentum and awareness underlying Social Impact Investing continues to grow, it adds a dimension to the future development of investment strategies and policy that is both exciting and challenging.

New investment architectural competencies will be needed to assist both families and foundations in navigating this increasing interest and alignment between investment goals and social contribution. The ever evolving opportunities and options, as touched on in this article, will require the development of well-defined and focused competencies and capabilities to provide the requisite support crossing all the disciplines of goals definition, strategic policy design, due diligence, and ongoing over-sight.

The response to these challenges will serve the continued transformation of the investment management industry to true goals-based and purpose-driven investing.

Sources

- RIA 2016 Canadian Impact Investment Trends Report, October 2016

- Principles for Responsible Investment 2016 Report

- Farthing-Nichol, D., and Jagelewsi, A., Pioneering pay-for-success in Canada, MaRS October 2016

- Impact Investing, Frameworks for Families, The Impact, January 2016

- State of the Nation: Impact Investing in Canada, MaRS Centre for Impact Investing and Purpose Capital

- Investor Manual, SVX Invest for Impact, Registered Dealer with the OSC

- Unleashing the Potential of US Foundation Endowments: Using Responsible Investment to Strengthen Endowment Oversight and Enhance Impact, US SIF Foundation

- Impact Investment: The Invisible Heart of Markets, Social Impact Investment Taskforce Established under the UK’s Presidency of the G8, September 2014

- Financing Social Good: A Primer on Impact Investing in Canada, an RBC Social Finance White Paper, June 2014

- From the Margins to the Mainstream, Assessment of the Impact Investment Sector and Opportunities to Engage Mainstream Investors, World Economic Forum, September 2013

- Impact Investing, A Framework for Policy Design and Analysis, Insight at Pacific Community Ventures & The Initiative for Responsible Investment at Harvard University, Sponsored by the Rockefeller Foundation, January 2011

- Mobilizing Private Capital for Public Good, Canadian Task Force on Social Finance, December 2010

- The State of Community/Mission Investment of Canadian Foundations, A Report of Community Foundations of Canada and Philanthropic Foundations Canada, by Coro Strandberg, April 2010

- Mission Investing for Foundations: The Legal Considerations, A Report of Community Foundations of Canada and Philanthropic Foundations Canada, Hunter, Manwaring, & Mason, November 2010, revised by Morin, July 2012

- Bugg-Levine, A. and Emerson, J. 2011 Impact Investing, Wiley Press, San Francisco

- Porter, M. and Kramer, M., Creating Shared Value, Harvard Business Review, January 2011

Websites

- un.org/sustainabledevelopment/sustainable-development-goals/

- https://iris.thegiin.org

- sustainalytics.com

- bcorporation.net

- impactinvesting.marsdd.com

- svx.ca

- riacanada.ca

- unpri.org

- https://thegiin.org

- http://impactassets.org

This family story is the third of a series in which we discuss some of the common investment challenges families face and what ultimately led them to HighView. Here, we explore what can happen when one member of an affluent family assumes responsibility for money and investments, particularly surrounding the concerns that can emerge as that person ages.

This family story is the third of a series in which we discuss some of the common investment challenges families face and what ultimately led them to HighView. Here, we explore what can happen when one member of an affluent family assumes responsibility for money and investments, particularly surrounding the concerns that can emerge as that person ages. In 2017, HighView proudly became a member of the Responsible Investment Association (RIA). HighView believes there is a fiduciary duty to invest prudently without taking undue risk. Incorporating Environmental, Social and Governance (ESG) standards into investment decisions to better manage risk and generate sustainable long-term returns makes sense. We believe ESG due diligence should be designed to measure how a company does business, to identify potential social and ethical issues, and to quantify the impact on corporate performance for disclosure purposes (i.e. better disclosure by companies should include climate-related financial disclosure).

In 2017, HighView proudly became a member of the Responsible Investment Association (RIA). HighView believes there is a fiduciary duty to invest prudently without taking undue risk. Incorporating Environmental, Social and Governance (ESG) standards into investment decisions to better manage risk and generate sustainable long-term returns makes sense. We believe ESG due diligence should be designed to measure how a company does business, to identify potential social and ethical issues, and to quantify the impact on corporate performance for disclosure purposes (i.e. better disclosure by companies should include climate-related financial disclosure). investment research and corporate actions. The integration of ESG considerations within investment processes and across asset classes continues to gain traction among investors and concerned citizens, both from the perspective of social impact, but also in the form of positive financial performance. While we had long known that our chosen managers integrated ESG criteria—particularly governance—into their investment process to varying degrees, we did not focus specifically on such practices.

investment research and corporate actions. The integration of ESG considerations within investment processes and across asset classes continues to gain traction among investors and concerned citizens, both from the perspective of social impact, but also in the form of positive financial performance. While we had long known that our chosen managers integrated ESG criteria—particularly governance—into their investment process to varying degrees, we did not focus specifically on such practices. A recent paper by SVX and MaRS suggests that many Canadian high net worth households are interested in the idea of impact investing, particularly younger, wealthier, and female investors. As Amit Bouri, chief executive of The Global Impact Investing Network (GIIN) says, “Investors have been thinking for decades on how to get harmful things out of their portfolios. Impact investing is about proactively investing in solutions. It is a much more intentional step about investing in things like climate change directly.” Impact investments are made with the intention of generating financial return plus positive social and/or environmental consequences. Examples of impact investment might include clean technology investments in agri-tech, energy, smart cities and water, or food in natural and organic foods, and ethical and sustainable foods, or in affordable housing, or helping people in poverty. There are a number of themes, sectors, geographies, and asset classes available to social impact investments.

A recent paper by SVX and MaRS suggests that many Canadian high net worth households are interested in the idea of impact investing, particularly younger, wealthier, and female investors. As Amit Bouri, chief executive of The Global Impact Investing Network (GIIN) says, “Investors have been thinking for decades on how to get harmful things out of their portfolios. Impact investing is about proactively investing in solutions. It is a much more intentional step about investing in things like climate change directly.” Impact investments are made with the intention of generating financial return plus positive social and/or environmental consequences. Examples of impact investment might include clean technology investments in agri-tech, energy, smart cities and water, or food in natural and organic foods, and ethical and sustainable foods, or in affordable housing, or helping people in poverty. There are a number of themes, sectors, geographies, and asset classes available to social impact investments. Our first speaker, Gayemarie Brown, embraces AI and sees abundant opportunity.

Our first speaker, Gayemarie Brown, embraces AI and sees abundant opportunity. Sri Iyer, Managing Director and Head of Systematic Strategies at Guardian Capital, and portfolio manager for the Guardian Global Dividend Strategy is one of HighView’s investment managers. Sri began his career in the financial services industry in 1995, firstly with Global Value Investors based in Princeton, New Jersey, and since 2001, with Guardian Capital.

Sri Iyer, Managing Director and Head of Systematic Strategies at Guardian Capital, and portfolio manager for the Guardian Global Dividend Strategy is one of HighView’s investment managers. Sri began his career in the financial services industry in 1995, firstly with Global Value Investors based in Princeton, New Jersey, and since 2001, with Guardian Capital. Another of HighView’s investment managers, Chris Page is President, CIO, and founder of Laurus Capital. Laurus relies on deep fundamental research and maintains concentrated portfolios of financially strong and well-managed companies with long term growth potential. For more than 30 years, Chris has held a number of senior positions within the investment and insurance business and founded Laurus with a vision of a firm focussed on client wealth creation through prudent risk averse investing and a culture that fosters independent thought.

Another of HighView’s investment managers, Chris Page is President, CIO, and founder of Laurus Capital. Laurus relies on deep fundamental research and maintains concentrated portfolios of financially strong and well-managed companies with long term growth potential. For more than 30 years, Chris has held a number of senior positions within the investment and insurance business and founded Laurus with a vision of a firm focussed on client wealth creation through prudent risk averse investing and a culture that fosters independent thought.

We are wealth architects whose sole purpose is to provide our clients with peace of mind by making their wealth sustainable.

We are wealth architects whose sole purpose is to provide our clients with peace of mind by making their wealth sustainable.